Asset Allocation

Optimization

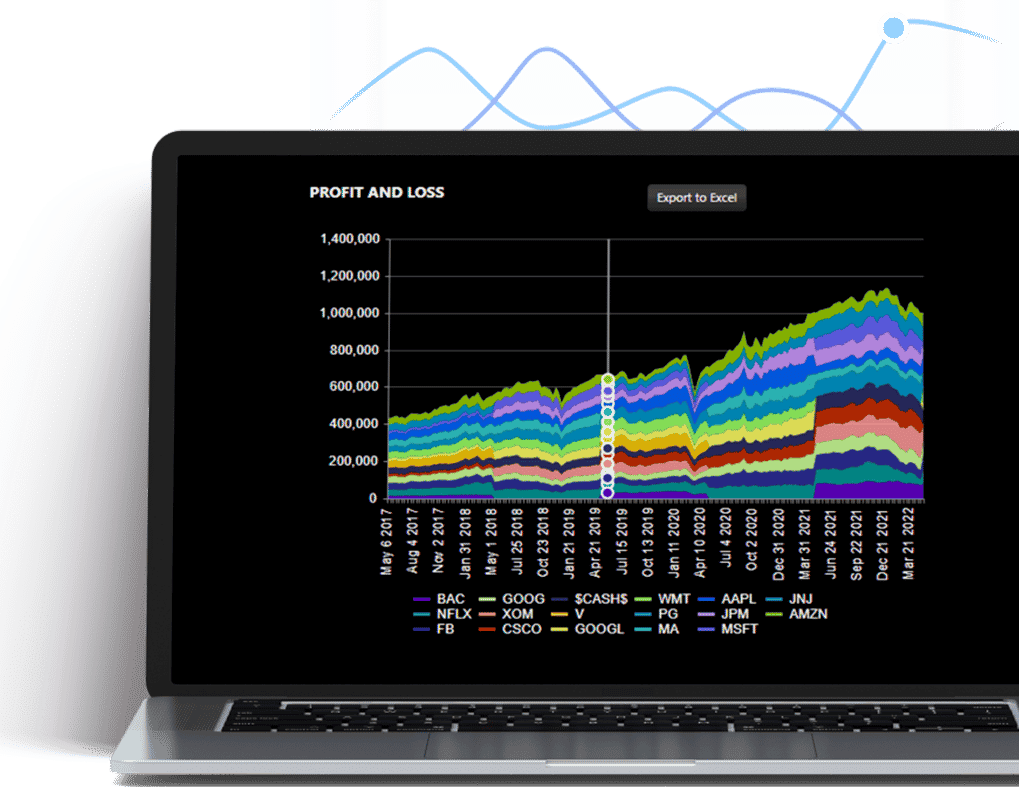

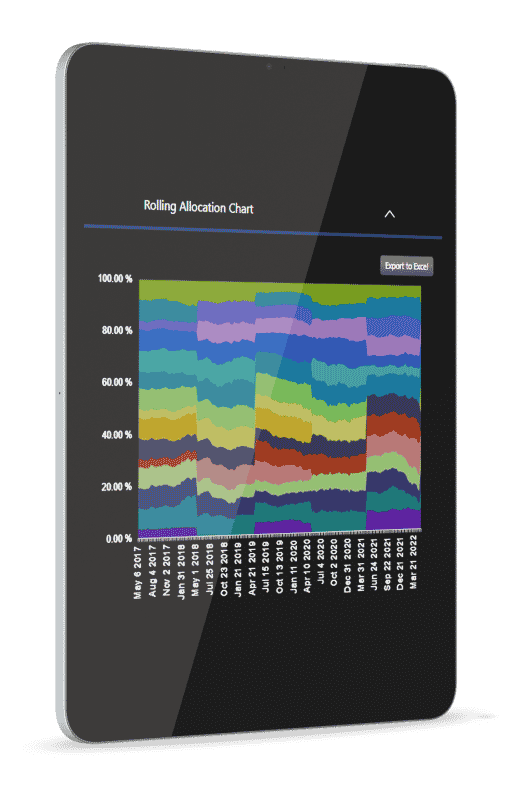

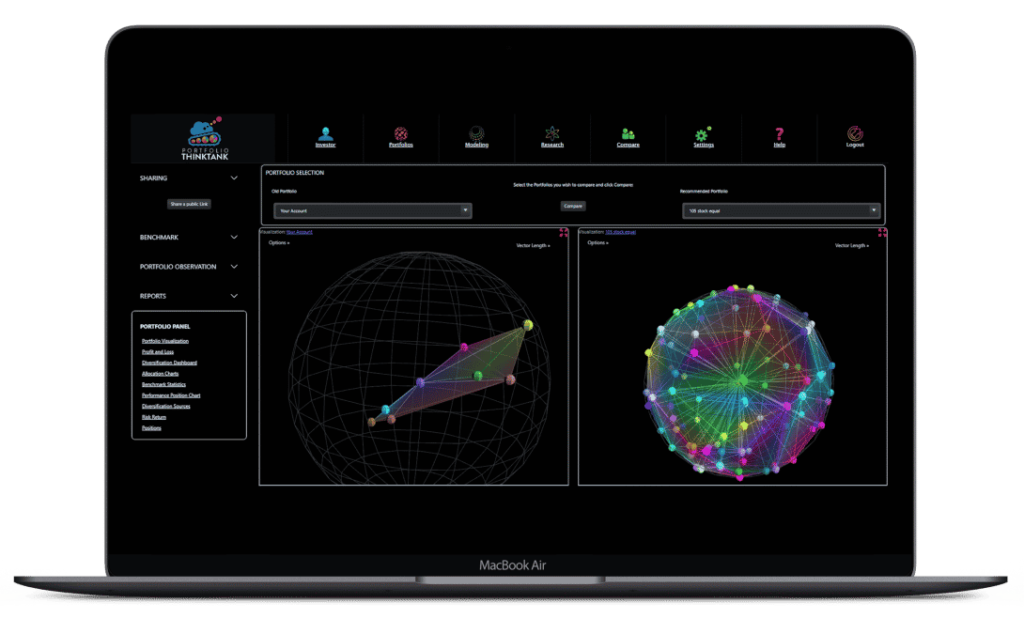

Portfolio Visualization

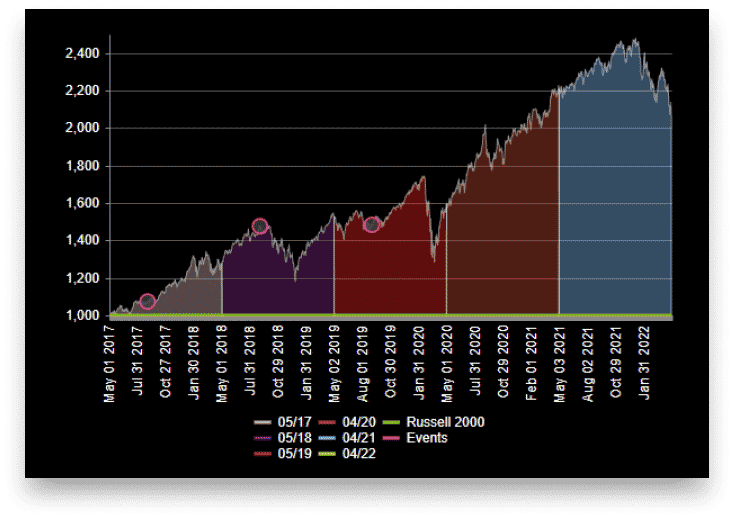

Re-Optimization

Backtesting

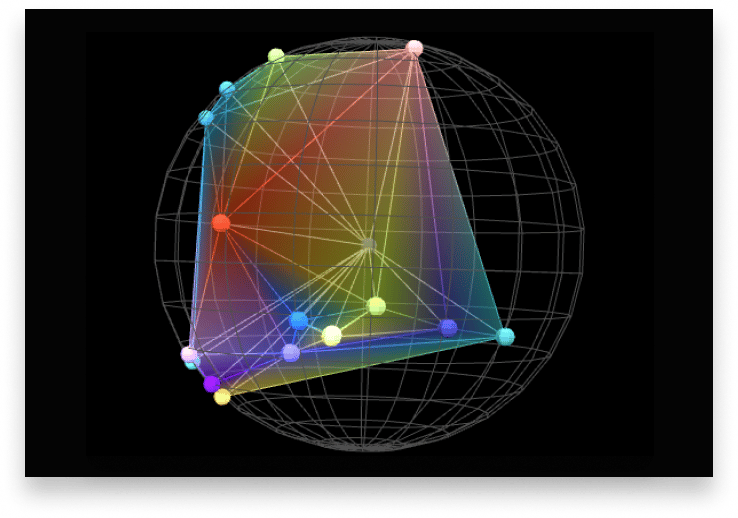

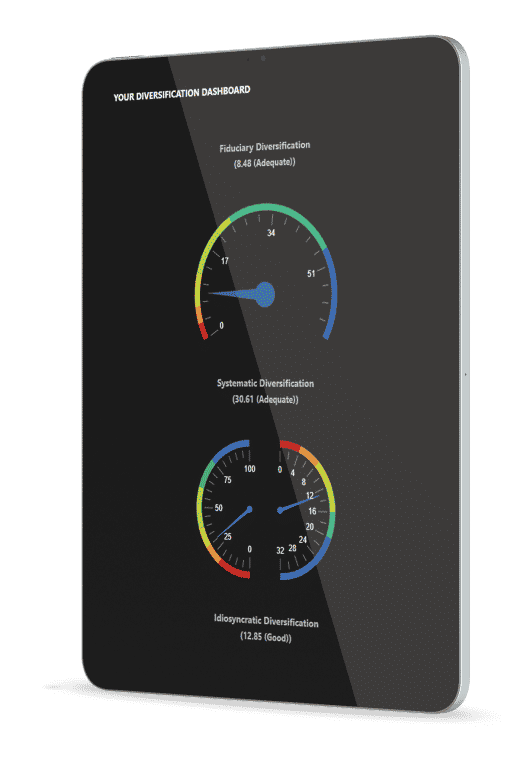

Diversification Analytics

Portfolio Visualization & Comparisons

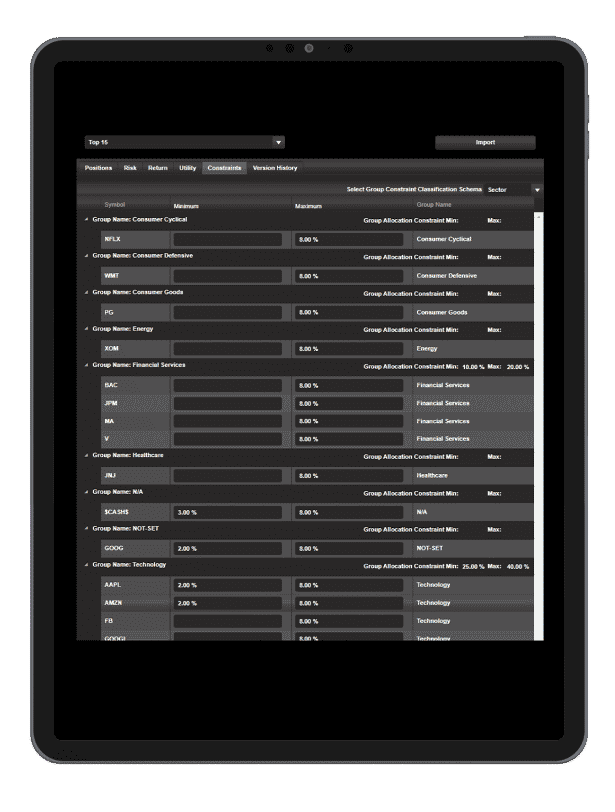

Constraints

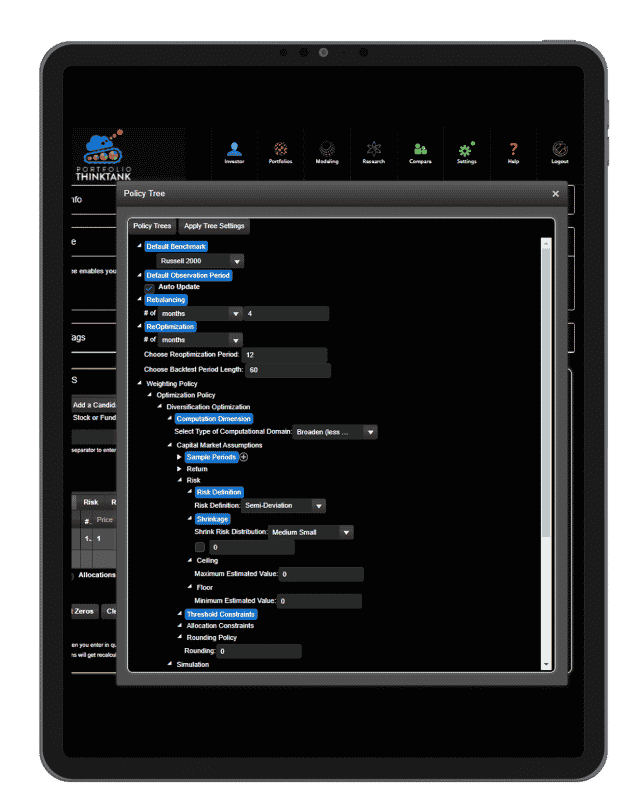

The Policy Tree

Jeremy J. Black

Founder and inventor of RAMCAP, the "intelligent asset allocator" one of the first desktop investment diversification systems; Former Adjunct professor to the College for Financial Planning; Co-Creator of one of the first "Fund of Funds" hedge funds - twice named in the top 10 by the Wall Street Journal.